|

Idea Generation: Swatch Group (UHR VX) has been the candidate selected in our short screener: "Cyclical losers/ headwind victims". The strategy/screener is based on identifying glamour stocks that are peaking in margins, deteriorating interim sales growth and CFO (cash-from-operations) and waning sentiment, This strategy has been backtested since 1993 to 2014 using cross validation (in and out of sample) with significant absolute and risk-adjusted performance metrics. The company: Swatch Group Ltd. (UHR VX) designs, manufactures, distributes and sells finished watches, watch movements, prestige watch components, electronic systems and luxury jewelry. UHR is led by G. Nicolas (Nick) Hayek, Jr., son of the late co-founder and chairman Nicolas Hayek. The company employs over 35,600 people in 50 countries worldwide.  Short Investment Rationale: The main reasons to be pessimistic upon UHR are pointed out below:

Short Position Risks: Some points why long-only investors could be attracted and squeeze short-sellers:

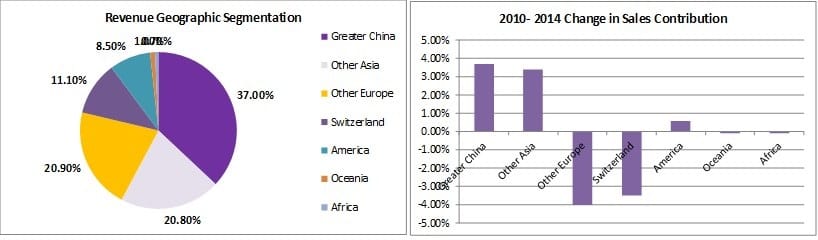

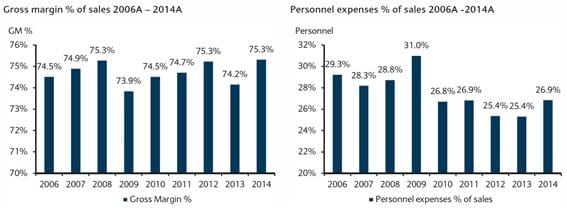

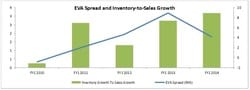

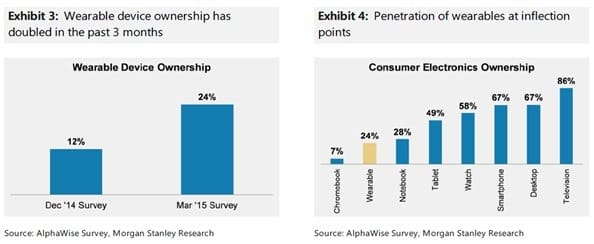

Key Insights Management overconfidence and China' new mindset about corruption China's government's stand against corruption has dramatically changed with luxury goods imports bearing double-digit negative growth rates. As a result, luxury peers have begun to slash prices in order to weather the storm, yet UHR management reluctance to follow peers eventually will impact its margins. This is a classic case of management overconfidence: last guidance figures were extremely optimistic with CEO reiterating 5-8% organic sales growth and 20% EBIT margin maintenance despite CHF strength, non-stop issues in China pricing and riding marketing & operating expenses. FX Tsunami: SNB action a one-off but is the last straw January was a turbulent month for Swiss stocks after the Swiss National Bank decided to terminate its policy of preventing the Swiss franc appreciating beyond SFr1.20 to the euro last week. The SNB move is a one-off action, yet inevitably it put things more complicated for UHR and plays a key role as the kick-off of an already weak company-specific and industry fundamental story. Peak in margins and increasing competitive intensity from Peers. The fine watches industry is a highly concentrated industry with Swatch Group, Richemont, Rolex and LVMH accounting for almost two-thirds of the $22bn Swiss watch market. After recent events such as the aforementioned clampdown on corruption in China and January's SNB FX action, most of the luxury watch brands - with the exception of UHR - have begun slashing prices in the country in order to adjust for both events.  UHR's peers have not negated reality - when the Chinese government policy on corruption changed or Crimea's crisis sparked a weaker Russian ruble - and marked down items gradually to avoid inventory piling and sudden margin deterioration. Regrettably, UHR has not even started to acknowledge this structural change as it can be seen in its balance sheet's increasing inventory-to-sales ratio and ramping inventory growth-to-sales growth. Last but not least, EVA deterioration over the last six months is a bad omen for the future and rules out any likely recovery in the short term.  Smartwatch wave: UHR lagging peers Global Smartwatch market has a potential to reach $32.9 billion by 2020, registering a CAGR of 67.6% during 2014 – 2020 or global wearables market will grow at a compound annual rate of 35% over the next five years according to BI Intelligence. Luxury watches are certainly a different animal when compared to smartwatches, yet some market share loss is inevitable as people discriminate or make choices about which item is more worth-wearing. UHR's Swatch Zero One (Summer launch) will be launched at a competitive price, 155 USD vs 349 USD iWatch Sport and core iWatch 550-1049 USD, yet it seems to be a very limited device in comparison to peers like Garmin, Fitbit or Apple. Last but not least, UHR's R&D budget allocation to compete in this arena has been shy in comparison to smartwatch peers, for which reason the most likely outcome is defeat. UHR management obvious choice should have been about acquiring an already smartwatch-focused player in order to save R&D and protect Watch's brand. Sooner or later UHR will have to capitulate.  To conclude, bearish momentum has grown significantly in Swatch Group shares and justify to open a short position on the back of company-specific issues, overall industry bearishness, FX macro shocks, increasing regulatory risks in its key markets and recent bear tactical signals: overbought RSI, bearish 50-200 MA, negative liquidity shocks and indulgent consensus. Disclaimer: the blog is intended to convey investment ideas and, market views , yet they are not a solicitation or recommendation to buy/sell/hold securities but merely investment ideas that should NEVER serve as the basis of the reader trading decisions. This website and its reports are for general information purposes and any investment decision should be discussed with a financial adviser before taking place. The investment ideas displayed here could have been implemented at an earlier date than the one stated at the blog's post date; for which reason the latter dates do not represent accurate and timely entry/exit points in order to protect those investors with whom the blog author has a fiduciary agreement.

0 Comments

Leave a Reply. |

Carlos Salas

LINKS Data Science & ML NYC Data Science Blog Data Science Central Towards Data Science Kaggle Blog Analytics Vidhya Quant Finance Quantocracy MoneyScience QuantStrat Trade R Investments Market Screner Macro Calendar Corporate Calendar Advisor Perspectives Trading Economics Portfolio Visualizer Datasets Opendata Data.Gov World Bank Quandl |

RSS Feed

RSS Feed