|

Idea Generation: "Growth Contenders" is a backtested screen delivering excellent results for the period 1993-2011 and 2001-2011 (excluding TmT Bubble irrational exuberance). The model has been trained and cross validated using different periods with multiple predictors using traditional variables (e.g, EPS growth) and dummy variables (e.g. cyclical or defensive sector). Among the different ideas screened, Mentor Graphics (MENT US) stood up as an interesting play. The company: Mentor Graphics (MENT US) is a technology leader in electronic design automation (EDA). The firm provides software and hardware design solutions that enable their customers to develop better electronic products faster and more cost effectively. MENT markets its products and services worldwide, primarily to large companies in the military and Aerospace, Communications, Computer, Consumer Electronics, Semiconductors, Networking, Multimedia, and Transportation Industries.  Investment Rationale :

Risks: Threats

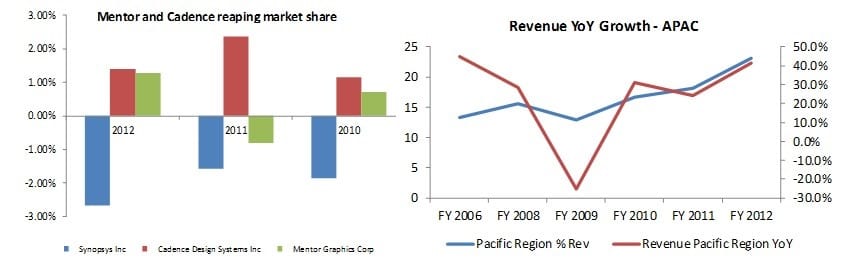

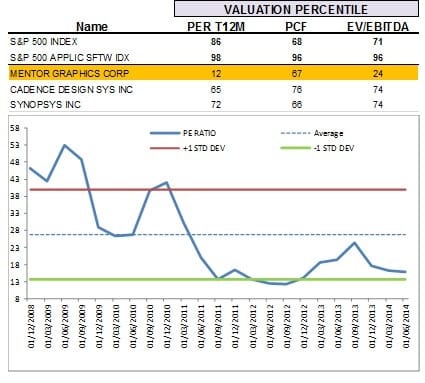

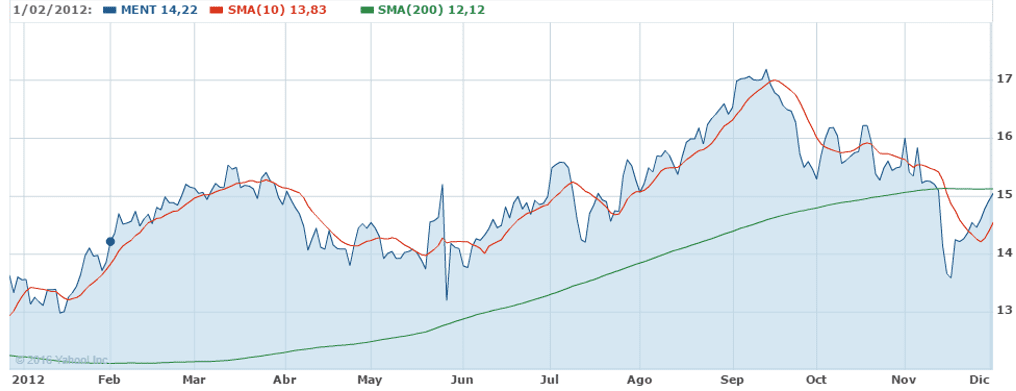

Valuation: Valuation levels are most attractive when looking at both EV/EBITDA T12M chart and Percentile Valuation table. We decided to leave out Price-to-Book, Dividend Yield and Price-to-Sales for several reasons. Firstly, Price-to-Book is not recommended to assess software companies’ valuation due to the complex exercise of discerning which goodwill is to be monetized in the future. Second, Dividends are not a cornerstone for these companies due to its focus on growth. Last, Price-to-Sales may be also rather misleading due to the comingled and diversified mix of revenue recognition policies practised by each one of the companies. Therefore, we opt for EV-to-EBITDA T12M, Price-to-Earnings T12M and Price-to Cash Flow. In this way, EV-to-EBITDA T12M is the traditional ratio to measure cheapness in M&A deals (Carl Icahn driver). Price-to-Earnings T12M is useful as to measure shareholder potential especially in low leverage levels. Moreover, Price-to-Cash Flow is also a nice tool to study how the firm cash generation capacity is rewarded by investors. MENT current price is around 15 USD tantamount to 12x PER T12M and 8.9 EV-to-EBITDA T12M. Under a conservative scenario where PER re-rates to 25th percentile or 16.5x, one shall expect MENT stock to soar towards 20 USD per share, using a very conservative next year estimated EPS of 1.22 vs 1.21 consensus. In other words, the potential upside is above +30% for the next six months. Bearish EPS momentum is gone and recent EPS momentum has experienced an upward reversal: the average quarterly EPS estimate has moved up from 16 cents to 21 cents over the last 3 months. For the year, analysts are projecting net income of $1.21 per share, which is still quite conservative.  An important short term resistance levels (15.12) was broken and the next level (16.50 or +16%) will be key for the bull trend to be persistent. The advice is to double exposure when either this level is broken . The flip side would come with the stock crossing back below 12.85 USD, which would be considered an advisable time to stop losses.  To sum up, Mentor Graphics is likely to capitalize and monetize prospects for EDA business in its stock price in the next three to six months. The company’s Asian exposure, competitive relative valuation to peers, latent M&A premium and mark-up power besides its low financial leverage, management’s long tenure and recent technical trading upward reversal signals are some of the reasons for being optimist about Mentor. Disclaimer: the blog is intended to convey investment ideas and, market views , yet they are not a solicitation or recommendation to buy/sell/hold securities but merely investment ideas that should NEVER serve as the basis of the reader trading decisions. This website and its reports are for general information purposes and any investment decision should be discussed with a financial adviser before taking place. The investment ideas displayed here could have been implemented at an earlier date than the one stated at the blog's post date; for which reason the latter dates do not represent accurate and timely entry/exit points in order to protect those investors with whom the blog author has a fiduciary agreement.

0 Comments

Leave a Reply. |

Carlos Salas

LINKS Data Science & ML NYC Data Science Blog Data Science Central Towards Data Science Kaggle Blog Analytics Vidhya Quant Finance Quantocracy MoneyScience QuantStrat Trade R Investments Market Screner Macro Calendar Corporate Calendar Advisor Perspectives Trading Economics Portfolio Visualizer Datasets Opendata Data.Gov World Bank Quandl |

RSS Feed

RSS Feed