"Framed" is a series of posts about behavioural finance where I like to delve into past investment mistakes, dig into behavioural bias specific topics and review related scholar and practitioner research. Human stock-pickers are prone to suffer from psychological mistakes and are always flagged by the media as an excellent turf to gather and analyze behavioral data. Nonetheless, one could say that lots of systematic machine learning models out there also suffer from a similar maladies such as overfitting, weak generalization, lack of flexibility, poor robustness or lazy model input feeding i.e. use of standardized inputs/predictors without carrying out a proper feature selection process. That said, Reinforcement Learning and other machine learning models are the future, especially in the trading arena where robots are unbeatable. But we are still not there in terms of finding an AI that can fully replace humans in terms of flexibility and capacity to detect nuances when running forensic accounting analysis and event driven insights, yet machines are helping humans to become more efficient and, ultimately, singularity will arrive to the event driven space. In any case, I think this post was a good opportunity to talk about some of my past mistakes and how a timely stop-loss policy, proper diversification and systematic risk management techniques are essential to protect a portfolio performance. Revisiting my trade log I found two interesting backfired trades that illustrate perfectly how behavioural erring impacts an ex-ante reasonable investment idea that had been previously shortlisted using systematically backtested screens: Long Valmont Industries (VMI US) VMI was filtered from our "Fundamental Value" backtested screen seeking candidates with extreme undervaluation and soft catalysts using predictors such as superior ROIC to peers, Industry-specific absolute and relative valuation cheapness, neglected company effect (low number of analysts, lowe but rising institutional interest), among others. After being filtered by our systematic screening (first stage) and rank very high in our quantamental scoring (second stage), VMI's bottom-up fundamental analysis was conducted:

Trade Autopsy:

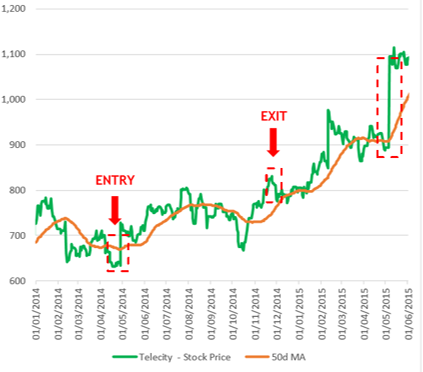

Short Telecity (TCY US) TCY was screend from our "Usual Suspects" screen aimed at identifying stocks with accounting red flags, stretched valuation and weak momentum. The screen was created from a backtesting carried out with data for more than 25 years while training, cross-validating and ensembling multiple models (random forest, XGB and logit mainly) with some factors/predictors such as accruals, off-balance sheet items (e.g. operating leasing, net Pension Liabilities), negative CFO growth, excessive goodwill & intangible assets compared to industry peers, issuance of debt to pay debt. TCY passed our first (systematic screening) and second stage (quantamental scoring) as one of the of the most promising short candidates. Ultimately, bottom-up forensic analysis was conducted on TCY with the next insights:

Trade Autopsy:

Behavioural mistakes: Conservatism Bias and Cognitive Dissonance

0 Comments

Leave a Reply. |

Carlos Salas

LINKS Data Science & ML NYC Data Science Blog Data Science Central Towards Data Science Kaggle Blog Analytics Vidhya Quant Finance Quantocracy MoneyScience QuantStrat Trade R Investments Market Screner Macro Calendar Corporate Calendar Advisor Perspectives Trading Economics Portfolio Visualizer Datasets Opendata Data.Gov World Bank Quandl |

RSS Feed

RSS Feed