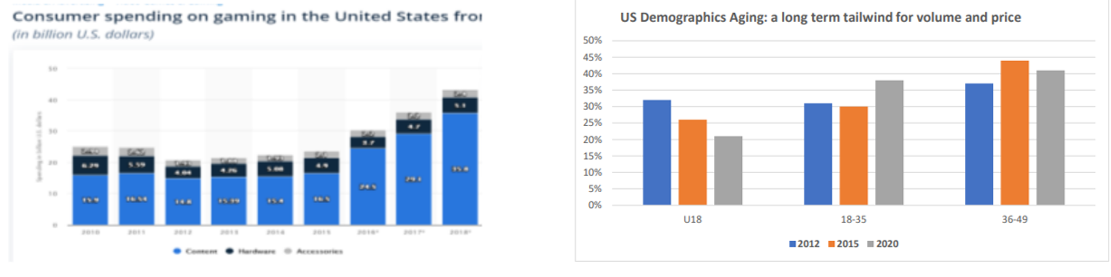

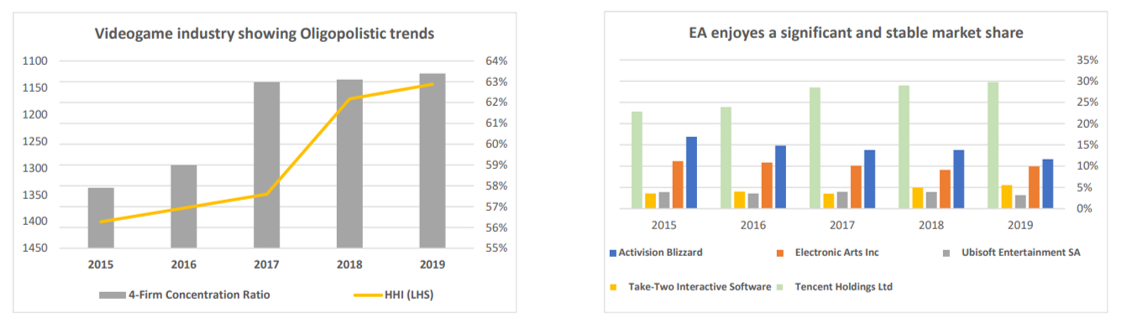

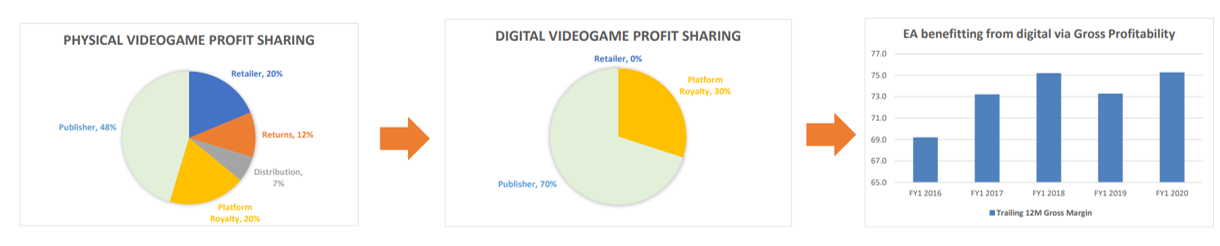

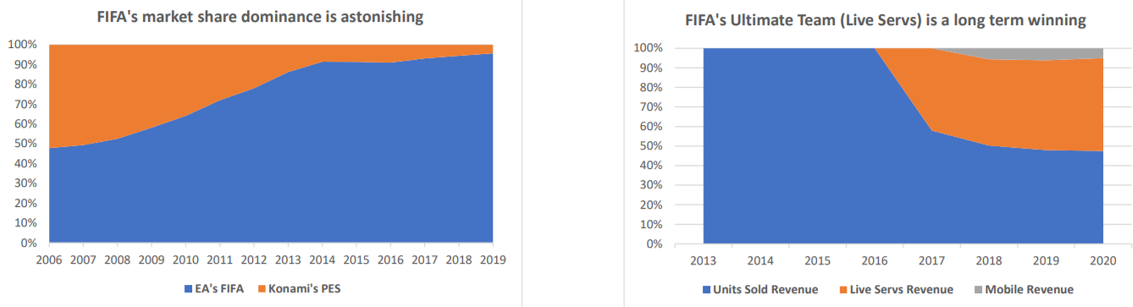

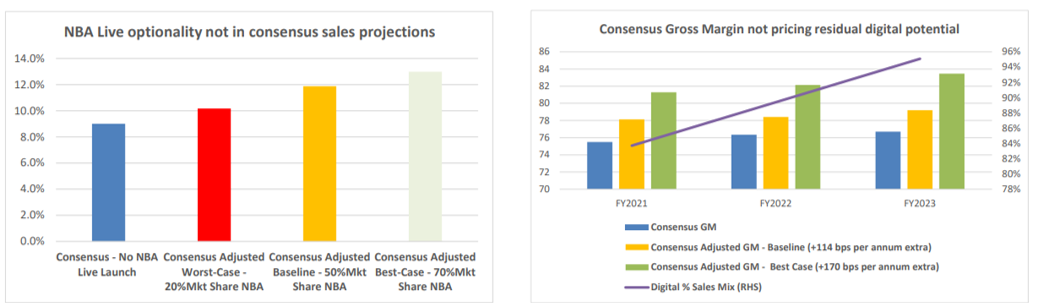

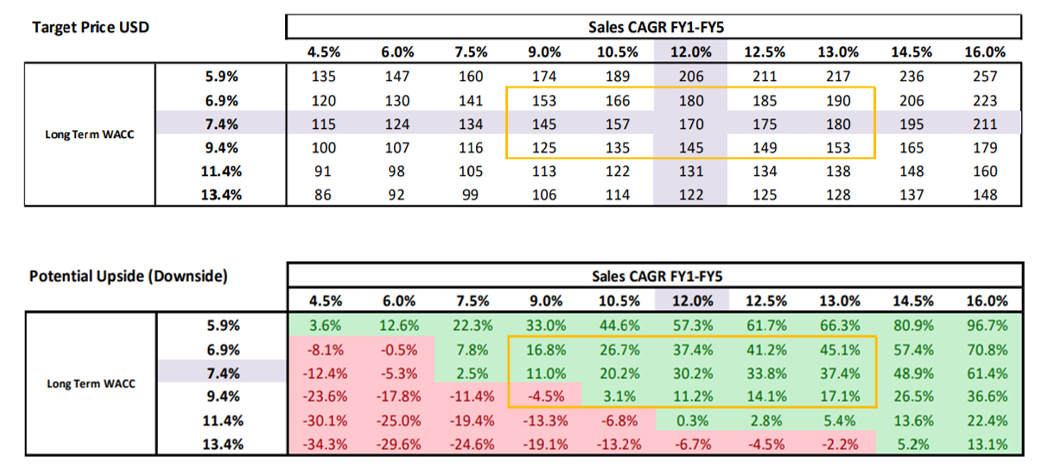

"Blend" is a series of posts with specific stock conviction cases showcasing how to combine multiple investing disciplines (machine learning scoring/screening, fundamental analysis, forensic accounting analysis, behavioural finance, corporate finance, alternative data) to generate differentiating alpha-generating ideas. Long Idea Key Takeways: Electronic Arts (EA) is a top player in the exciting videogames industry ($150bn TAM, +9-13% CAGR 2020-2025) with multiple secular drivers (demographics, digital transition, subscription model), short term catalysts (Covid19, NextGen launch), and company-specific unique traits like its sports franchise, a strong in-house and licensed portfolio of franchises, an increasingly exposure to e-sports, and consensus projections not pricing important information that all combined makes EA an attractive high-quality growth stock. Demographics are an unstoppable megatrend with two sources: gamer aging and developing markets: The average US gamer age has increased from 30 years old in 2012 to ~40 years in 2020 (source: ESA). This gradual ageing process will continue along with an increase in gaming expenditure per capita (+15%-20% CAGR). Another demographic advantage is the increasing income per capita in developing countries with increasing access to technology. EA will also expand more aggressively into new geographies with substantial demographic appeal such as Latin America and India.  EA is top 4 position with a stable market share in an oligopolistic industry. An analysis conducted using the top 18 public-listed videogame developers excluding platform builders (Nintendo, Microsoft, Sony) confirms the shift towards an oligopolistic status i.e. 4CR(4-firm concentration ratio) flashing “oligopoly” status increasing from 58% to 63% since 2015. Another popular metric used by the US DOJ is HHI (Herfindahl-Hirschman index) soared from 1143 to 1400 during the same period confirming the transition towards “soft oligopoly”. Nevertheless, one of the most important effects that both metrics don’t factor is the degree of bargaining power gained with clients on the back of the fall of the brick & mortar distribution (e.g. Gamestop) and the advent of the digital distribution over the last decade. In this way, EA’s market share has been stable and able to grow stronger and adapt over the last three decades:  The fall of the “brick & mortar” model and the advent of digital distribution is a boon for EA. EA’s digital sales segment has soared from 38% in 2013 to 78% in 2020 with gross margins increasing in the same period from 63.5% to 75.3%. On the back of the digital migration, EA has been able to attain +170 bps in gross margins per year (+30 bps for every additional 1% of digital sales migration). In other words, assuming EA goes fulldigital at the same pace thanks to Covid19, there’s a potential to expand margins by +170 bps per annum for a cumulative gross margin expansion of +650 bps for the 2021- 2026 period, or +114 bps per annum (+440 bps cumulative) under a more conservative scenario. Moreover, the new subscription-based model has increased EA’s quality and revenue visibility from an investor standpoint. EA’s Live Services (subs, updates, microtransactions, etc) grew at +26.2% YoY pre-Covid19 and +50.4% YoY post-Covid19 in 2Q20 (FQ1 2021) confirming EA’s success is not pandemic-dependent. Lastly, EA recently acquired Gamefly’s cloud gaming assets that could allow in the next decade to become independent from any platform and fully embrace the streaming megatrend.  NextGen launch driving volumes and higher prices per game. The standard price for video games is increasing to $70 (+16.7%) for NextGen console launches (PS5 and Xbox) ending 15 years of $60 games. EA’s rival TTWO was the first to move with the announcement that NBA 2K21 will cost $60 for current generation consoles but $70 for next-gen consoles. Moreover, Sony announced $70 pricing for some PlayStation 5 launch games in September. This is great news for EA as it leaves the firm a lot of leeway to decide about its pricing policies going forward. EA also plays an interesting role in an impact investing mandate. Since reaching a low point in mid 2010s, EA has been on a mission to rebuild its reputation with stakeholders (racial justice sponsorship, antibullying campaign, 75% reduction in microtransactions, EA originals hub seeding independent development teams including former employees). Over the last couple of years the firm has improved dramatically in Glassdoor overall rating (3.9 vs 3.2 2018) compared to close peers ATVI (3.2 vs 3.9 2018) and TTWO (3.7 vs 4.2 2018). In addition, Sustainalytics ESG shows EA ranking significantly high at 77.73 compared to TTWO (30.25) or ATVI (42.85). The most important contribution of EA from an impact investing standpoint is the creation of media content aimed at promoting diversity principles to engage with its heterogeneous gaming audience. Lastly, research to date suggests videogames can improve an individual’s attention, visuospatial ability and enhance medical therapies as long as playing time is limited to less than 2 hours per day (average gamer 0.9 hours per day). EA sports series and other valuable licensed IPs are a differentiating factors against peers. Sports titles generate predictable revenue, gamers addiction and less development costs than non-sports projects. FIFA is the crown’s jewel (~40% revenue) with FIFA20 becoming the top seller during lockdown times and reaching an astonishing dominance in football games (96% market share vs 50% 2007). Another opportunity overlooked by consensus is NBA Live 2022 launch. NBA Live series was cancelled two years to focus on delivering a next-gen top-notch title that could compete against TTWO’s NBA2K franchise but news in 2021 of the franchise re-launch will provide a strong catalyst in the shares. Furthermore, EA signed a 10-year collaboration deal with Disney (Start Wars), a long term collaboration with FIFA (1993) that will renew in 2022 and a similar situation with other parties (NHL, NFL/Madden) that have no reasons to abandon EA thanks to the significant popular and economic success of these licensed franchises (65% total revenue) for more than a decade. Beyond sports, EA has generated its own IPs with franchises such as Battlefield, Skate, Apex Legends, Sims, Need for Speed, or Mass Effect with non-sports titles generating an average 40% of total revenue.  Esports megatrend is here with with lots of optionality for EA in the long term. Esports is only a $1 bn niche in 2020 with revenue from merchandise, event tickets, sponsorships, advertising, and media rights (less than 1% total videogame industry), but expected to grow +15-25% CAGR for the next decade. EA is behind rivals such as Riot Games’ LoL, Valve’s Counter-Strike or Activision Blizzard’s Overwatch League (all of them with formal esports leagues), yet FIFA is the main esport tournament with a remarkable potential to grow. EA is the top winner in terms of indirect benefits to direct sales from esports according to niche experts and sell-side analysts whereas there’s an untapped potential for EA’s sports series to conquer esports. Covid19 tailwinds on social distancing (short run) and generational impact (long run) Social distancing measures will linger in FY20-21 and impact positively gaming revenue. Steam data reflects a global PC gamer base 20% larger than pre-Covid19 levels. Bear in mind a Covid19 situation lasting beyond 2020-2021 could echo in the gaming habits of new generations (e.g. GenZ) with sell-side analysts expecting 2%0-30% of the newly acquired gamers and pre-Covid19 gamers new habits to remain in a post-Covid19 world for at least two decades. Activist optionality: inefficient capital structure, cash surplus and lack of dividend. The company credit metrics are rock solid with a meaningful cash balance of $ 5.7bn (~10% Market Cap) and negative Net Debt ($-4,7 bn). The business is a reliable cashflow generator growing at +30% 3YR CAGR (FCF Margin 32.5% vs 30% Peers) with no forensic accounting red flags, minimal intangible impairment risk (17% Assets vs 50% ATVI) and superior R&D profile ( 30% Sales vs 15% ATVI or 8.8% TTWO). In fact, a significant majority of shareholders driven by activist groups voted against the company's executive compensation plans a couple of months ago (Harvard Business School research shows "say-on-pay" votes have failed only less than 3% in the last decade). In other words, activist investor groups are using peer ATVI’s case (0.5% dividend yield) to start a tug of war against the management team’s reluctance to share a dividend that will eventually put some pressure on EA’s executive team to improve shareholder yield in exchange for a positive “say-on-pay” vote in the 2021’s shareholder meeting. Consensus ignoring NBA live franchise reboot and digital migration’s residual margin expansion. TTWO’s NBA 2K20 generated +$1 billion in combined sales and microtransaction revenues worldwide (14 mill units, $71.42 per unit) despite gamers’ complains on microtransactions and several glitches, yet there was not another NBA choice in the market. EA’s reshuffle of its NBA live franchise in 2022 could provide that alternative for NBA fans with new features like WNBA female players attracting women’s interest (50% game players nowadays) or loyal NBA live fans coming back. The chart below shows several scenarios for NBA Live’s market share that could add a significant momentum to EA’s 2022 consensus revenue projections but that will be kicking in into the shares in 1H21 as news about NBA Live 22 development are released. This along with the previous comments on gross margin profitability residual upside within the next 5 years as digital continues to increase in importance are the two main levers not priced in today’s consensus projections for 2021 and 2022.  EA valuation not pricing multiple structural tailwinds and short term catalysts. EA’s valuation is remarkably cheap on a relative basis against both global and US-based peers using a 5-year valuation ratio window. For instance, EA’s Forward PE discount to global peers as of 5th October is 10%, which is in stark contrast with the 5-year average premium of +10%. The market is not accounting for some catalysts mentioned in this report looking forward 2021-2022, besides favouring more aggressive videogame stocks (higher exposure to low-margin mobile) despite EA’s better fundamentals as Covid19 times present a significant tailwind for the industry. The significant revenue visibility gained over the last decade, future secular trends and EA’s healthy free-cash flow margin generation profile are good reasons to use a DCF model to assess different valuation scenarios. The next baseline inputs are used: +12% 5-year CAGR (NBA Live 22 launch assumption not discounted in consensus +9% CAGR), +440 bps gross margin expansion (conservative compared to +650 bps potential), 6.5% WACC, 7.4% WACC long term and a reasonable 2% long term growth rate. Even when not factoring previously mentioned tailwinds (e-sports optionality, NextGen higher pricing, activist optionality, long term Covid19 effects), the shares display a good entry opportunity at below $125 per share as of 6th October 2020 with the “highly likely” squared area highlighting mostly a range of positive scenarios:  EA Long Thesis Risks:

Long Trade Management:

Disclaimer: the blog is intended to convey investment ideas and, market views , yet they are not a solicitation or recommendation to buy/sell/hold securities but merely investment ideas that should NEVER serve as the basis of the reader trading decisions. This website and its reports are for general information purposes and any investment decision should be discussed with a financial adviser before taking place. The investment ideas displayed here could have been implemented at an earlier date than the one stated at the blog's post date; for which reason the latter dates do not represent accurate and timely entry/exit points in order to protect those investors with whom the blog author has a fiduciary agreement.

0 Comments

Leave a Reply. |

Carlos Salas

LINKS Data Science & ML NYC Data Science Blog Data Science Central Towards Data Science Kaggle Blog Analytics Vidhya Quant Finance Quantocracy MoneyScience QuantStrat Trade R Investments Market Screner Macro Calendar Corporate Calendar Advisor Perspectives Trading Economics Portfolio Visualizer Datasets Opendata Data.Gov World Bank Quandl |

RSS Feed

RSS Feed